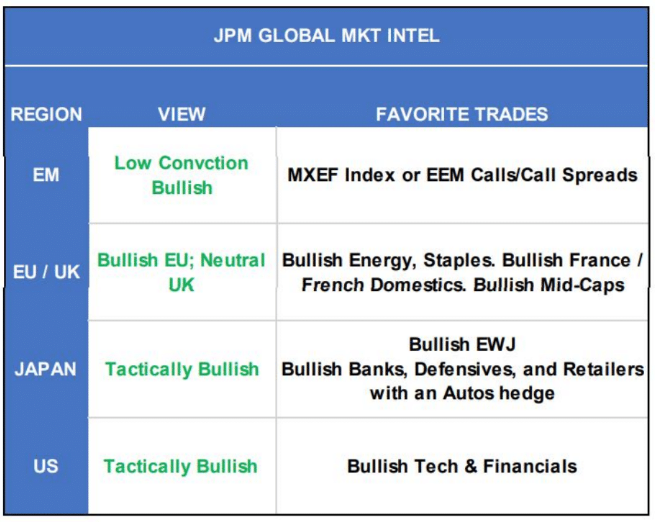

Institutional Insights: JPMorgan CPI Scenario Analysis

.jpeg)

JPMorgan CPI Scenario Analysis

For CPI, the forecast for Headline MoM is +0.30% and for Core MoM is +0.23%, both consistent with market expectations. This translates to a YoY increase of 2.9% for Headline and 3.1% for Core. If these figures hold, it would mark the lowest Core CPI reading since April 2021. The subsequent scenario analysis represents a perspective from the JPM US Market Intelligence trading desk. We are examining Core MoM results and 1-day SPX reactions.

For a scenario where MoM outcomes are 0.40% or higher, we could see a sharp rise in Shelter costs and a shift in some Core Goods from deflation to inflation (such as Household, Medical, and Alcohol). Expect a strong reaction in the bond market as it adjusts to a view that Fed Funds won't be restrictive, with the likelihood of the Fed taking action to hike rates rather than cut them. Such a change in bond yields would likely push the USD higher, putting additional pressure on stocks. Anticipate the NDX to excel while the RTY lags behind. SPX could fall between 1.5% to 2%.

For outcomes between 0.33% and 0.39%, the reaction might be more influenced by rising goods prices than services, leading to a tempered response in the bond market but a similar effect on stocks. This print may not completely eliminate all expectations of interest rate cuts for FY25, but it could potentially create uncertainty about the likelihood of one cut in FY25. As of last Friday, the bond market is pricing in about 37.5bps in cuts.

For the scenario where outcomes fall between 0.27% and 0.33%, it represents a base case showcasing a modest MoM increase, aligned with a trend upwards observed since September, reflecting an overall uptick in inflation amid improved growth and hiring, albeit potentially at a slower pace. Bond yields are expected to stay within a range, leading to a favorable scenario for stocks. This situation may not be precisely “Goldilocks,” but due to the market's resilience year-to-date, stocks could rise, especially RTY contributing to growth. SPX may either lose 25bps or see gains of up to 1%.

For outcomes between 0.21% and 0.27%, this scenario is considered “Goldilocks,” particularly if paired with robust Retail Sales data. The market would likely fully price in two cuts anticipated this year, with equities responding positively, primarily driven by SMid-caps, with SPX gaining between 1% and 1.5%.

[5.0%] 0.20% or lower. The other possible outcome involves a decrease in Shelter as Core Goods turns net deflationary. In this scenario, bond yields would steepen, leading to RTY significantly outperforming SPX. The USD is likely to react negatively, benefiting EM Equities, which are anticipated to outperform RTY. SPX is expected to gain between 1.25% and 1.75%.

WHAT DOES OPTION PRICING SUGGEST? Options expiring on Wednesday are indicating a move of roughly 1.3%, based on the closing prices from Friday.

US MARKET INTELLIGENCE - On Friday, the market reacted excessively to the Univ of Michigan data, in our opinion. This has led to an undue focus on the CPI figures. Our perspective on the economy continues to suggest above-trend GDP, positive EPS, and a neutral Fed with a dovish inclination. A slightly stronger print could challenge that outlook but also heightens the risk of US inflation due to a potential comeback from China, especially if that revival is supported by more considerable-than-expected fiscal measures.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!