The US Dollar Rallies as Mixed CPI Report Sparks Inflation Debate

The latest US Consumer Price Index report has once again placed inflation concerns front and center in the minds of market participants, especially within the currency markets. Released data for August reveals mixed signals regarding inflationary trends in the US, causing immediate reactions in the US dollar and investor sentiment. The headline inflation fell slightly to 2.5% year-on-year, lower than July’s 2.9% and marginally below expectations. However, the core CPI, which strips out the volatile food and energy components, ticked up by 0.3% monthly, slightly above July’s 0.2%.

This combination of factors—softening headline inflation and a more resilient core figure—has stirred the pot in terms of interest rate speculation. Prior to the release, market consensus was growing for a 50-basis point rate cut by the Federal Reserve at the upcoming Federal Open Market Committee (FOMC) meeting. However, the unexpected uptick in core inflation has reignited debates over the Fed’s next move.

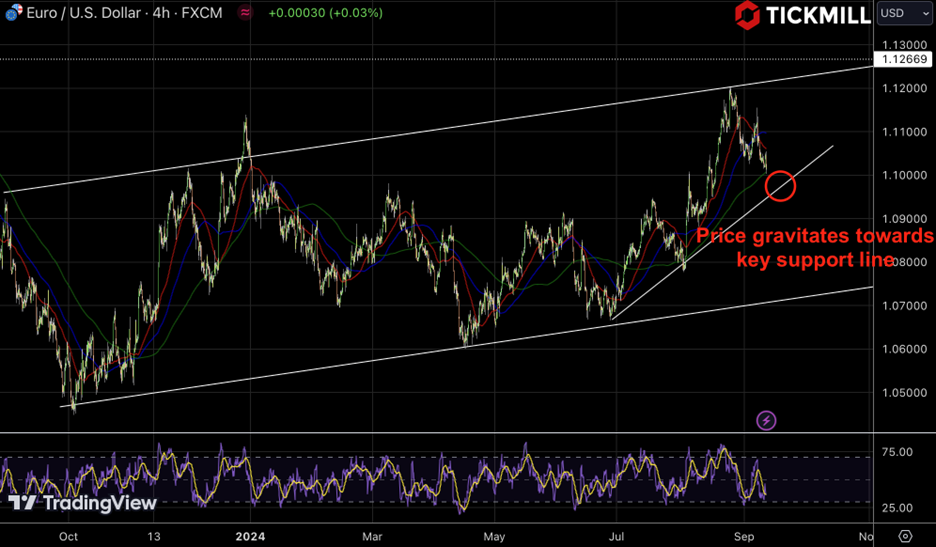

The immediate impact on the US dollar was a surge in strength. The currency quickly rallied, bolstered by rising expectations that the Fed might take a more cautious approach toward rate cuts. EURUSD was pressured and apparently targeting breakout of 1.10 level as concerns persist that the ECB may deliver another bearish surprise on Thursday:

Interest rate derivatives, which gauge market sentiment on future Fed policy actions, show a 67% chance of a 25-bps rate cut next week, as opposed to a 50-bps cut, which now seems less likely. Should the Fed decide on a smaller cut, this would likely signal that policymakers are more concerned about inflationary pressures than previously anticipated, lending additional support to the USD.

In the broader macroeconomic context, a strong USD could suppress exports, as US goods become more expensive for foreign buyers, potentially weighing on US economic growth. On the flip side, a strong dollar could ease import price pressures, helping to moderate inflation further down the line.

Across the Atlantic, all eyes now shift to the European Central Bank meeting, where policymakers are grappling with their own set of challenges. With growth in the Eurozone, particularly in Germany’s manufacturing sector, slowing dramatically, the ECB is expected to announce a 25-bps cut to its deposit facility rate. This move aims to stimulate growth in an economy that has been increasingly weighed down by external factors, including global trade tensions and sluggish domestic demand.

Despite these anticipated measures, the outlook for the EUR/USD pair remains uncertain, and the near-term risks are skewed towards downside, reinforced by the technical setup mentioned above. If the ECB also revises down its growth forecasts—something many market participants see as a real possibility—the Euro could face additional selling pressure. This would further limit any upside in the EUR/USD, which has already given back gains made earlier in the week.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.