Institutional Insights: Goldman Sachs Positioning & Sentiment Update

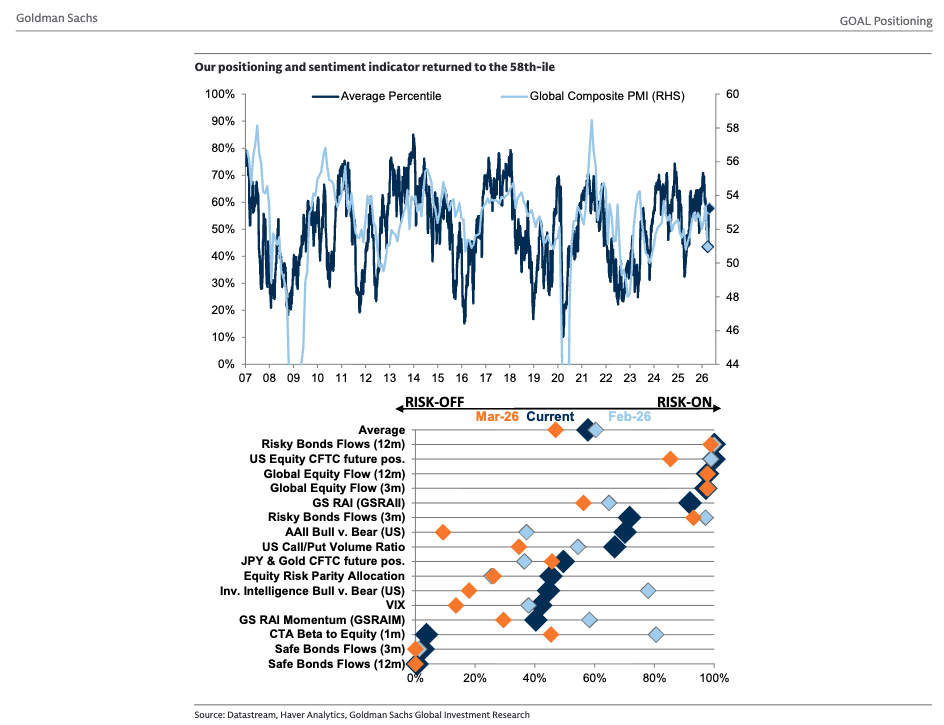

Sentiment & Positioning: Risk Appetite Has Recovered, But the Re-Risking Is Uneven

Our Sentiment and Positioning Indicator has rebounded to the 58th percentile, while our Risk Appetite Indicator is now back to pre-war levels at 0.79. The improvement is clear in derivatives and flow metrics: call-put ratios have surged, equity vol has reset sharply lower, and the market has moved away from pricing aggressive tail-risk scenarios. This normalization is also reflected in the decline in cross-asset skew, as investors have reduced demand for downside protection and rotated back into higher-beta assets.

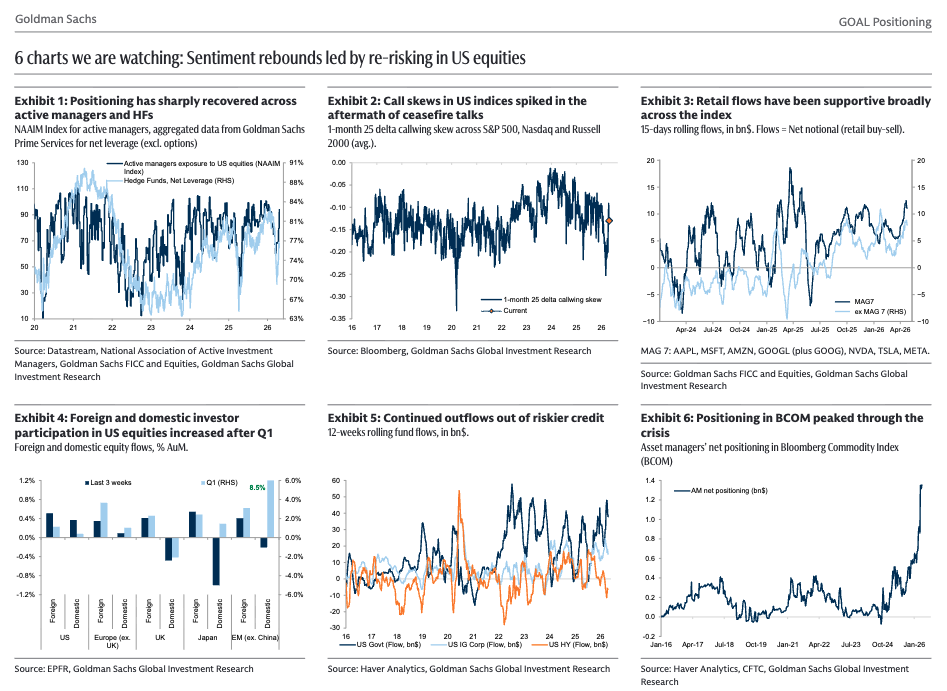

The equity rebound has been especially sharp, with US indices leading the way. Following the ceasefire, US equity call skew surged, pointing to renewed demand for upside convexity and stronger risk appetite. At the same time, S&P 500 put-call ratios fell to historically low levels, supported by broad-based retail buying across the index. The rally also benefited from several positioning tailwinds, including continued US retail inflows, systematic buying from CTAs, risk-parity and options strategies, and renewed re-leveraging by US asset managers and hedge funds.

Regionally, the US remains the main destination for incremental equity risk. Since Q1, both foreign and domestic investors have primarily added exposure to US equities. Outside the US, domestic demand for local equity markets has generally slowed. By contrast, US investors have significantly increased allocations to both domestic and foreign equities. Notably, roughly half of the approximately $100bn in US domestic equity inflows year-to-date were committed in just the last four weeks, underscoring how concentrated the recent re-risking impulse has been.

That said, they have not uniformly re-risked. Investors have been more careful with cyclicals and leveraged funds in recent weeks, which suggests that the rebound is being driven more by targeted equity risk and upside optionality than by a broad macro rotation. Outside equities, investors have shown a more modest recovery in risk appetite. Earlier this year, government bonds and investment-grade credit dominated inflows, while high-yield credit has recently seen renewed outflows. Credit sentiment indicators have improved from the stress levels seen a few weeks ago, but they remain less emphatic than the equity signal.

In FX and commodities, safe-haven demand has moderated. Dollar strength implied by risk reversals has partially faded, while safe-haven positioning has eased through sharp outflows from gold ETFs and a decline in JPY futures positioning. Commodity exposure, however, has moved in the opposite direction: asset manager positioning in BCOM futures has risen to its highest level on record, reflecting both renewed inflation-hedge demand and the direct impact of the energy shock.

Risk appetite has recovered meaningfully, and equity positioning has rebuilt quickly, particularly in the US. But the setup is no longer cleanly one-way: upside demand is strong, volatility has compressed, and retail/systematic flows have helped power the rebound, while cyclicals, leveraged funds and high-yield credit show a more selective and cautious re-risking impulse. The market is back in risk-on mode, but positioning is now less washed out and more vulnerable to disappointment.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!